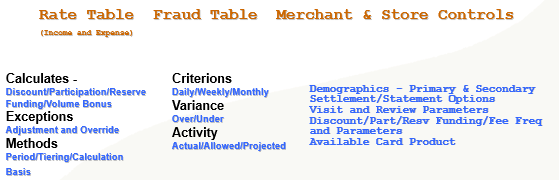

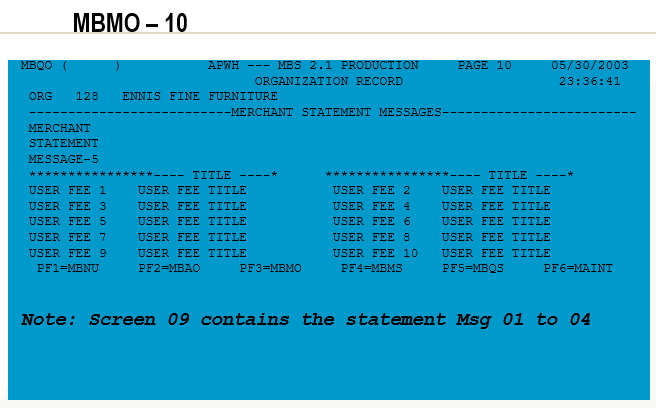

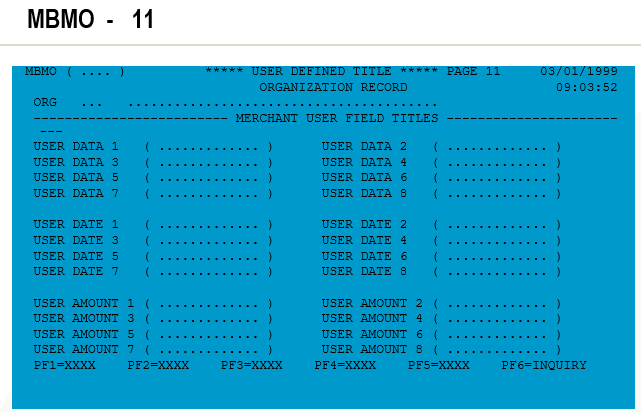

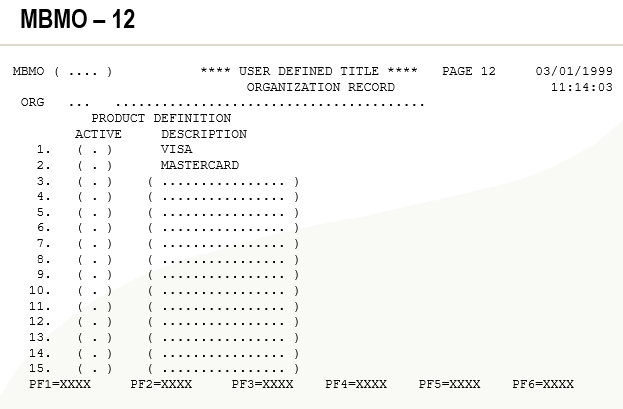

At Org level 5 stmt messages can be defined. On Merchant level any one or more of these can be selected to be populated on the merchant statements. MBS allows nearly 46 system fees and 10 user fees. For user fees the title can be defined at org level. This titles are displayed in the merchant statements. At the merchant level 8 user dates, 8 user amounts and 8 user data are allowed. The title of all this fields ( to be shown on corresponding screen ) can be assigned at the org level. On the MBMO12 screen, 99 valid products with their status at the org level can be defined. Any merchant within this org can use only the active products within this org.

Let us take a look at Loyalty management system (LMS) popularly known as ‘Rewards’ system.

It is a system designed to allow card issuers to build a base of loyal customers by rewarding them with points or cash-back rebates according to their use of their card.

This is a VisionPLUS subsystem which presents a consistent look and feel as other VisionPLUS modules to maintain ease of use for operators and end users.

It is parameterized and enhanced (over CMS Frequent Shopper functionality) to provide maximum flexibility and tailoring from one loyalty scheme to another.

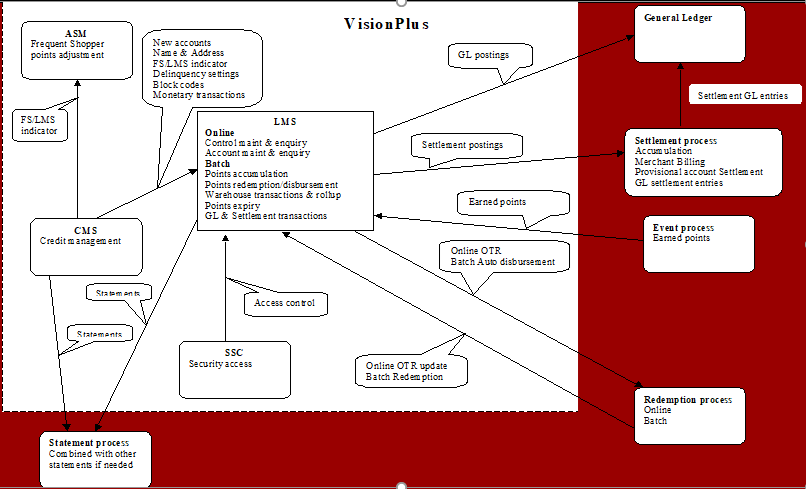

LMS System architecture:

LMS System Architecture

Online Control Record (System, Organization & Scheme records) setup Account setup, Name locate Points Balance inquiries, Transaction History Add/Maintain/Inquiry of Points transaction CICS callable function to allow external access by third-party redemption systems Batch Non-monetary maintenance Points calculation and posting Expired points processing Auto-disbursement Reporting Redemption Transaction file Event Based non-monetary Transaction file. Account Status

Interfaces Accepts incoming monetary transactions from CMS(AR System) Accepts incoming non-monetary user input to add and maintain master file data in the new Loyalty system Accepts incoming non-monetary transactions files from a third party source to allow event based processing Accepts incoming points transactions for Loyalty accounts from a Third party redemption system. Creates outgoing General Ledger transactions Creates outgoing Settlement file Creates outgoing file of points that have been redeemed Creates outgoing file of information to support the production of customer reward statements by CMS / Statement system Provides a real time interface to a third party redemption system

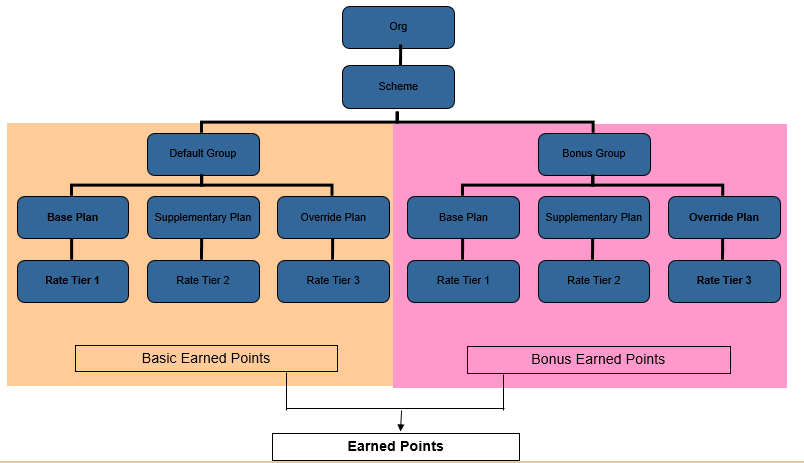

What is Scheme?

A loyalty Scheme is required to attract the account volumes required to create a substantial and profitable portfolio. The Loyalty Scheme will define the basic parameters regarding the earning, redemption and expiry of points.

What is scheme structure ?

An Account can be enrolled into multiple Schemes. Loyalty Scheme Name field allows greater flexibility when setting up scheme (as it is five alphanumeric field). All the accounts will have at least Default group. Both type of groups can have three types of Plans – Base, Supplementary & Override.

Scheme Structure

What is a Group ?

There are 2 types of Groups in LMS: The default group of all ‘A’s is defined for each Scheme and controls the basic earned points awarded to an account and settlement with the Provision Account.

Default group Organization specific.

Each Store is linked to Default Group (as a minimum) to generate Basic Earned Points.

Bonus Groups control the allocation of bonus points to an account and settlement with the merchant.

Multiple Stores participating in a Bonus Rewards Scheme constitutes Bonus group.

A Store can be associated with multiple Groups

What is a Plan ?

LMS defines three types of points for each Group attached to a Scheme: Base points that are allocated to a loyalty account as part of the standard features and offerings of the loyalty program. Supplementary points that are offered in addition to the base points for a specific promotion/period. Override points that are offered instead of the base and supplementary points. This could be used to offer double points for the month of November each time the card is used.

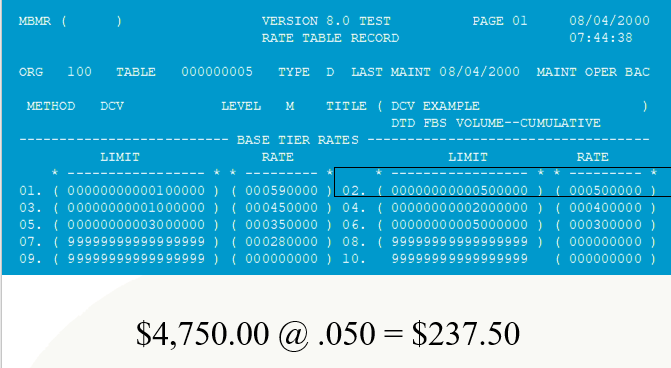

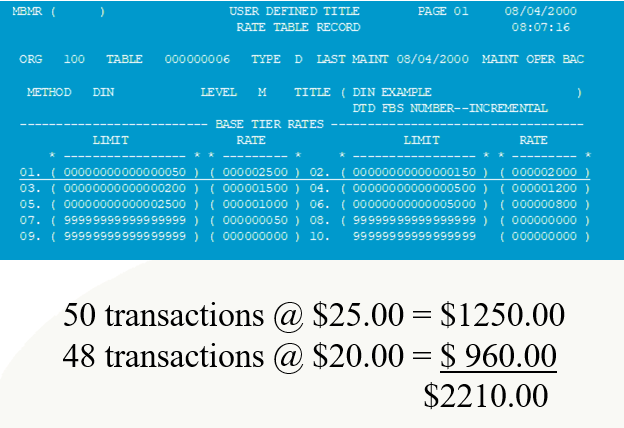

Rate table & Rate Tiers:

Allows to determine and to vary the ratio of points assigned to a transaction at the points Scheme level based on the monetary value of the transaction. Provides a facility to enter a minimum value that must be present to qualify for a point. Bonus point definitions (Bonus Groups) have the option to define different rates.

Enrollment:

New accounts can be setup automatically from an external interface, such as CMS/ CDM/SNAP, or directly from within the Loyalty system using online transactions. Possible to add new accounts on a daily basis through the Loyalty system batch process.

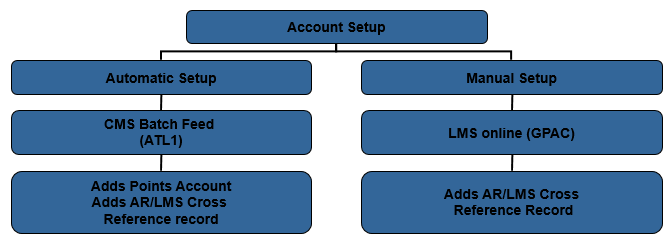

Enrollment

LMS can generate account numbers automatically. In Automatic mode, record is added in Account cross reference file, LMS Demographic data file and Points account file. In Manual Mode also LMS account no. can be generated automatically. Manual Setup can be used for creating multiple LMS accounts for One AR account. AR/LMS Account Cross reference file will have to be updated manually (QPAX).

Account maintenance:

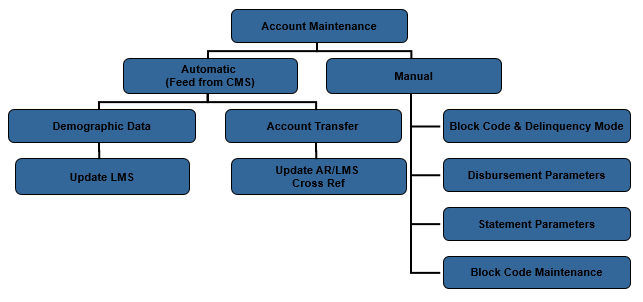

Account details can be maintained either via an external interface, typically from CMS, or via online maintenance within the Loyalty system.

LMS automatically handles account transfers without the need for manual processes in Loyalty.

Account Maintenance

Adjustments:

Allows an operator to add, maintain or inquire upon batches of Point transactions. The following types of transactions can be entered from these screens Basic earned Points (debit or credit) Bonus Points (debit or credit) Redeemed Points (debit or credit) Adjustment Points (debit or credit) Manual Redemptions and redemption reversals.

Online transactions will be rejected online if If the account is blocked or delinquent, or for manual redemptions when the Open to redeem is less than the transaction amount he transaction will be rejected online. Batch of ‘Adjustment Transactions’ is processed in the LMS batch. If expired points need to be reinstated, the point’s adjustment transaction can be generated.

Redemption:

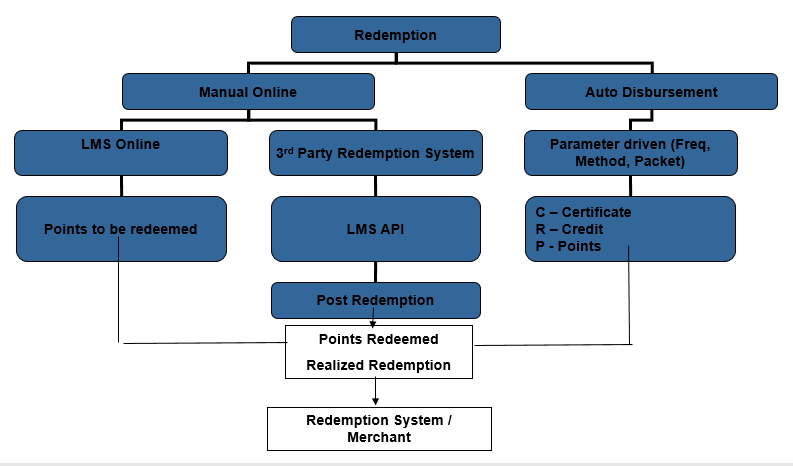

Redemption is the ability to allow a customer to redeem points. The points are redeemed in exchange for products or services Oldest points will be redeemed first. Accepts incoming file from a third party Redemption system The block codes & Delinquency associated with the AR and or LMS account is checked before approval is given for redemption.

Redemption Process

Online Redemption thru LMS can be done using Points Adjustment Function. For 3rd Party Redemption System, there is standard Record layout. Auto Disbursement Frequency can be set to determine the time of disbursement. An AUTO DISBURSEMENT METHOD parameter will allow the operator to specify the method of disbursement, Check, Credit or Certificate (Voucher). Auto Disbursement Packet can be set. It is the number of points automatically disbursed, if the account’s available points balance is greater than or equal to this number of points. If the value is Zero then all points will be disbursed.

Provides the ability to define the number of days before points will become eligible for redemption after being received by the Loyalty system, using the warehouse facility. Facility to determine whether the Cycle to Date points are to be included or excluded from the Open to Redeem Points calculations. No matching off process will take place between outstanding redemptions and incoming redemptions. It will be the responsibility of the third party Redemption system to provide a file of realized redemption points to the new Loyalty system.

Settlement:

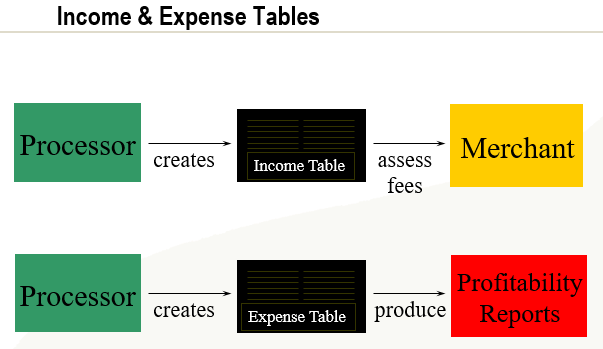

It is a financial settlement that occurs between the Loyalty points funding participant, Issuer, and the Redemption channel. Merchant Settlement Merchant settlement is the process whereby the Merchant is charged for participating in Loyalty Schemes. Merchants can be charged for Bonus points and can be charged at the group or store level. LMS allows to define: Merchants, both group and store level. Merchant settlement accounts. Rate charged. Expressed as a percentage. Settlement methods available will be Direct Debit, Invoice or both

Redemption Settlement Redemption settlement is the mechanism to pay Redemption merchants for services received by the financial institution on behalf their cardholders throughout the selected redemption period. LMS allows to define: Redemption settlement accounts Settlement with different redemption merchants at settlement intervals Different dollar rates for redemption merchants. Manual adjustment of redemptions for settlement purposes.

General Ledger:

For each points transaction processed, a monetary equivalent is calculated and then posted to the

General Ledger. LMS allows to define : General Ledger account numbers for debit and credit accounts for every monetary value processed by the system. a percentage rate for the monetary equivalent value of a point and tax rates applicable. Two sets of General Ledger entries are produced during LMS processing: Provisioning : Provisioning GL relates to the scheme owner putting money aside to cover the cost of points. Merchant Settlement : Merchant Settlement GL relates to requesting money from participating merchants for points awarded for customer transactions originated through the merchant.

Settlement General Ledger : LMS will produce a single settlement GL file containing general ledger entries for merchant settlement for inclusion into the third party General Ledger System.

LMS allows to define : Debit and Credit GL Accounts Rate Percentage. The rate at which points are equated to a monetary value.

The provisioning General Ledger entries are system generated as a result of point’s calculation processes within LMS.

They represent monetary commitment for the points earned.

LMS allows to define : Transaction code and description Debit and Credit GL Accounts Rate PCT Tax Rate for provisioning General Ledger

Transaction History:

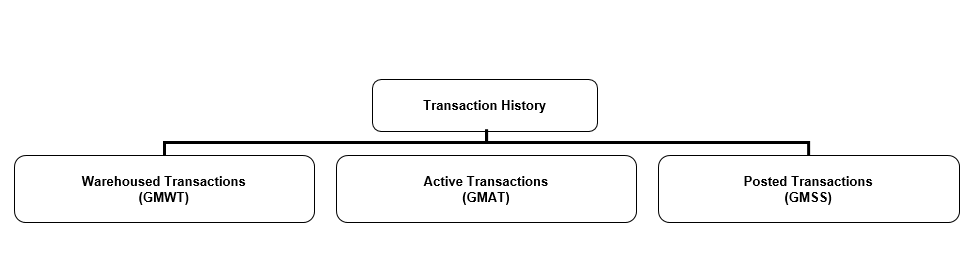

Transaction History

Warehouse transactions – this screen will display all monetary transactions where the points are yet to be calculated and posted.

Active transactions – this screen will display the point transactions that have been calculated and posted but either the account has not statemented and/or the transactions have not been settled

Transactions history – this screen will display all point transactions that have posted, statemented on the loyalty account and settled with the merchant

Wildcard search feature (*) is allowed.

Transactions can be searched for on account number, Scheme, Merchant DBA, Merchant Id number, batch number, batch date or AR account number.

Period between Expiry of Points & Removal from the Transaction History file can be specified for a Scheme.

Switching is a centralized dedicated software system, which is overall controlling the different functionality which starting from capturing of data (messages) of the monetary transaction and non- monetary transaction through different channel and route it to the different entities.

Capture and Route

Capturing transaction and Routing to different entities (Authoriser).

Examples of Switch – Electra, Open to Switch

End to End processing

Customer to Distribution

There are different phases in the Acquiring and Switching

Captures of the data through different channel.

Receive of the different message in a central Transaction Management entity.

Storage of all the messages in a central Database

Depending on the type of transaction; ON-US or NOT ON-US transaction routing to correct destination.

Depending on the Bank, a Switch can be an Acquiring Switch or Issuer Switch. If the message capturing through different channel is excluded for the other phases like Transaction Management and Routing part, the rest can be form the part of the Issuer switch.

Phase I

Capturing through different channel

Capturing monetary transaction in different channel

ATM

– Whenever an ATM is set for the first time/ there is change is accepting which all cards can be accepted, a down load file is being sent/ receives from the ATM and Switch.

Based on the type of the card, a OPCODE is being generated and as per that the screen are displayed; if it is a ON-US card then number of facility are provided to the card holder; other wise up to Authorization, only few functionality will be provided to the card holder.

– 1 OPCODE = 8 keys

– There is a one to one connection between the switch and ATM.

POS

Different POS are connected to the NAC (Network Access Control)

Data is sent from POS to NAC by means of (TPDU –Transaction Packet Data Unit)

POS uses the protocol Rs 232/x25

Example of the POS –Hyercom, Visacheck, Visa1

e-Merchant

-Merchant logon to the website through which he connect to the Web Server which in turn connect to the Payment Gateways – which again connect to the specific Interchange – again get connect the specific Acquirer id.

IVR

Mail Order Telephone Order –MOTO

Interactive Voice Recognition (IVR)

Local Networks

Phase II

Transaction Management ( Routing to different entities; based on the ON-US and NOT ON-US transaction)

CMS and HCS work together to provide commercial card processing and reporting. HCS provides management of the company structure and account creation as well as reporting in the form of organization level reports and interfaces to Master card Smart Data and VISA INFOSPAN.

The structure of HCS depends on a business’s organizational chart. Each entity in HCS is considered a “node”. A node could be a company, a cost center, or an individual account. A company can have up to 99 levels and up to 999,999,999 reporting units which could be representative of a division, department, cost center etc. HCS can also support up to 999 products (CMS Logo).

Company Node – Highest level in the HCS hierarchy. The company node contains node information that defaults from the Company Master record.

Reporting Node – Node or “entity” representing an intermediate level in the company hierarchy, such as a specific division or cost center. This type of node contains name and address information to identify the business unit that is represented. These nodes serve as reporting unites and track summary account information

Account Node – Represent individual accounts and are attached to reporting nodes. This node is always the lowest level of the hierarchical structure, but can be attached to any reporting node, regardless of level. An account node can represent an actual cardholder, or it can represent a billing account used by CMS sweep processing provides the account processing and passes transaction and account information to HCS.

The Hierarchy Company System (HCS) is an application that provides a company hierarchy structure for processing commercial cars and managing the relationship between the company, the sublevel reporting within the company, and the individual commercial card accounts.

HCS supports multiple hierarchical levels, multiple card products, statement processing, reporting, letters, and transfers for each company.

HCS interfaces to the Credit Management System (CMS) to obtain transaction activity and provide accounts-receivable information.

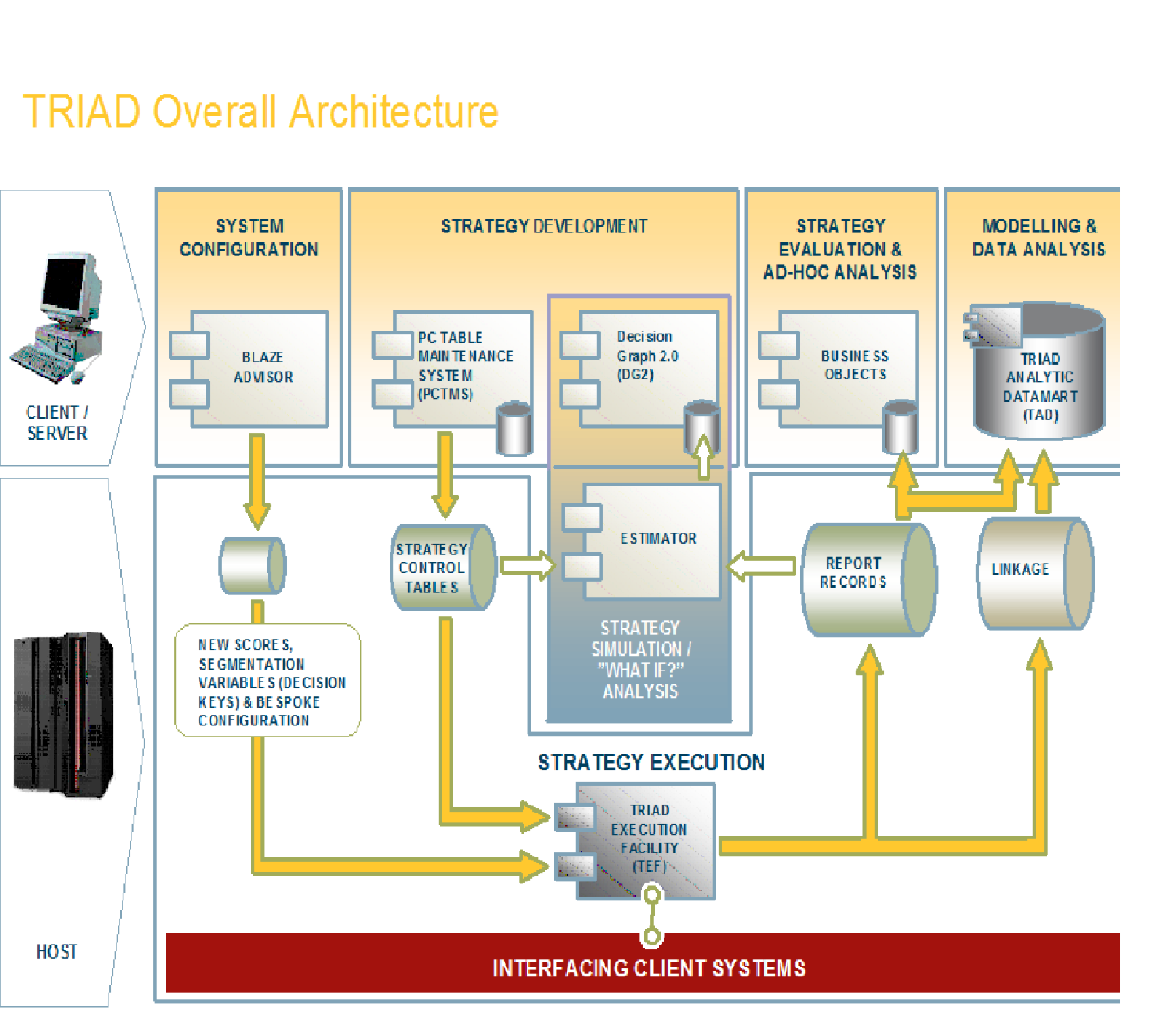

FICO® TRIAD® is the world’s leading credit and deposit customer risk management solution, helps deliver profits. TRIAD’s closed loop decision improvement process drives long-term profit growth at lower risk through a unique combination of analytics, simulation, champion/challenger testing, and unmatched strategy consulting. More than 65% of all customer credit card decisions worldwide are automated and improved with TRIAD.

Credit card processing companies, like other companies, must make a profit or go out of business. To achieve this goal, they charge fees.

These fees can be numerous. This can lead to some irritation. As in: What is all this stuff?

In the belief that knowledge is power, heres a quick breakdown of what all that stuff is.

Application Fee

Generally speaking, reputable companies do not charge this fee. They dont need to. They get enough business without charging up-front. Application fees are, by and large, bogus.

Startup Fee

Some work is involved in setting up a credit card processing account. A startup fee in the range of $25 can be justified, as long as the system thats set up works great.

Statement Fee Credit card processing companies usually provide detailed statements at the end of each billing cycle. These statements show how many credit cards were processed, the times and dates of the swipes, good stuff. The organization of that information has value. So they charge for it.

A statement fee of seven to ten dollars per month is common.

Monthly Minimum Credit card processing companies take a percentage of each transaction, so if no transactions are occurring, theyre not making any money. For this reason, they may put a andquot;monthly minimum not metandquot; charge into the contract. That way, they are assured of some revenue from each account.

Discount Rate

The discount rate is the primary fee charged by credit card processing companies. It is customarily between 1.5 and 2 percent of each transaction.

Charge Back Fee

Refunds complicate matters. If credit card transactions are repeatedly being charged back and forth, and the credit card processing company is being asked to void transactions after the fact, and so on, a charge back fee may occur.

Often, a certain number of charge backs are allowed per month before this fee kicks in.

Gateway Fee

This fee is related to the ability to process Internet credit card transactions. In order to do that, a credit card processing firm must provide some basic Web site services, such as a shopping cart function for the customer and/or a portal that lets the client accept and monitor payments.

A gateway fee in the neighborhood of ten dollars per month is common.

Termination Fee

Typical contract lengths are between one and three years, with early termination fees ranging from one to three hundred dollars. There are credit card processing providers who do not charge a termination fee. However, that may mean they charge a bit more in other areas.

How Much Is Too Much?

As a general rule of thumb, processing credit cards is a great deal if the cost is at or around two percent of total credit card purchases. If $100,000 of credit card purchases flow through a restaurant per month, processing credit cards might cost $2,000 per month.

When offers are flying around at less than that, be wary. Remember: credit card processing companies have to pay fees too, to the credit card companies themselves.

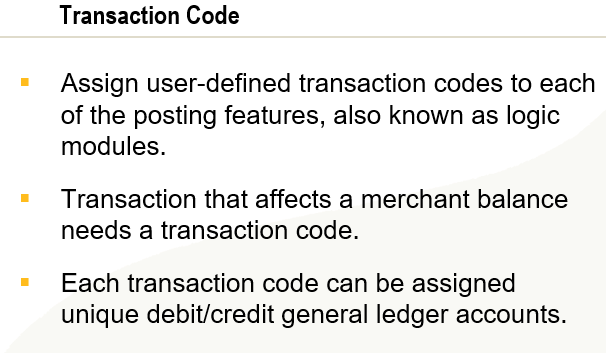

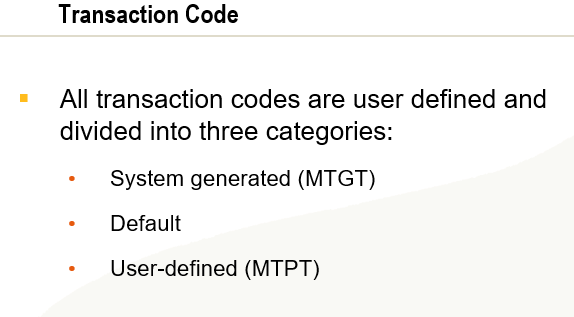

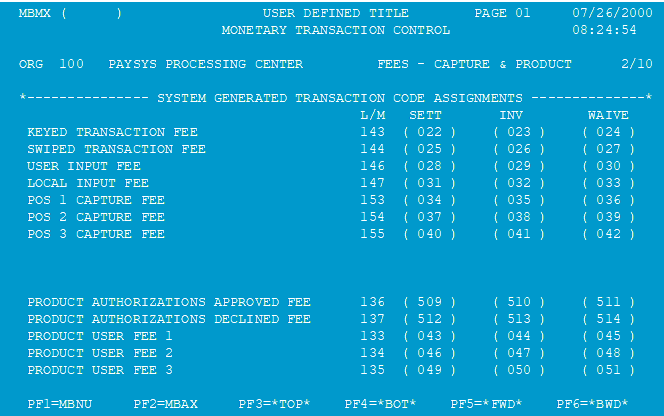

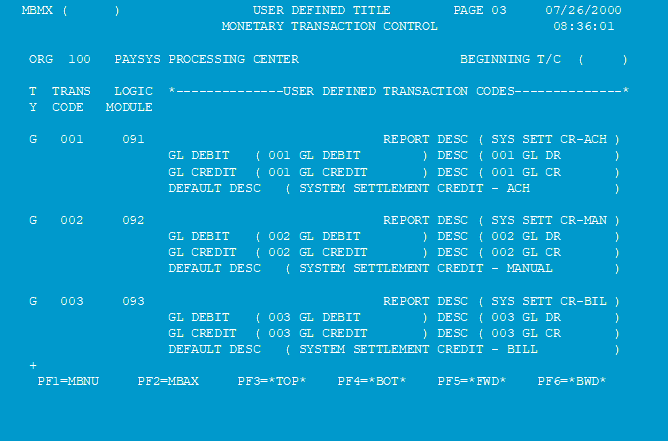

For each monetary transaction code you define, you must establish corresponding debit

and credit general ledger account numbers. You can define a General Ledger record for

each organization you process. If you prefer, you can establish the General Ledger record

at the logo, store, or credit plan master level within an organization. This level must

correspond to the general ledger reporting level you defined on the Organization record

(GENERAL LEDGER REPORTING LEVEL fields on ARMO03). For example, if you select the

option to report your general ledger at the store level within an organization, you must

enter the valid organization and store numbers on the General Ledger record.

For each organization established in CMS, you must define a set of general ledger account

numbers for the reporting level defined on the organization. You can also assign a unique

reporting description to each monetary transaction using the General Ledger record.

During batch processing, CMS verifies that the required general ledger entries have been

completed before balancing the daily job stream.

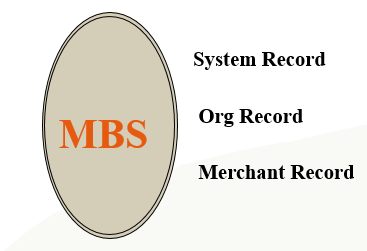

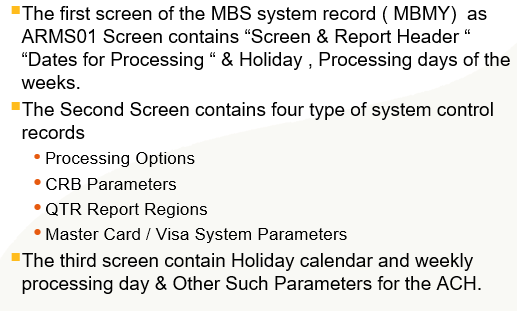

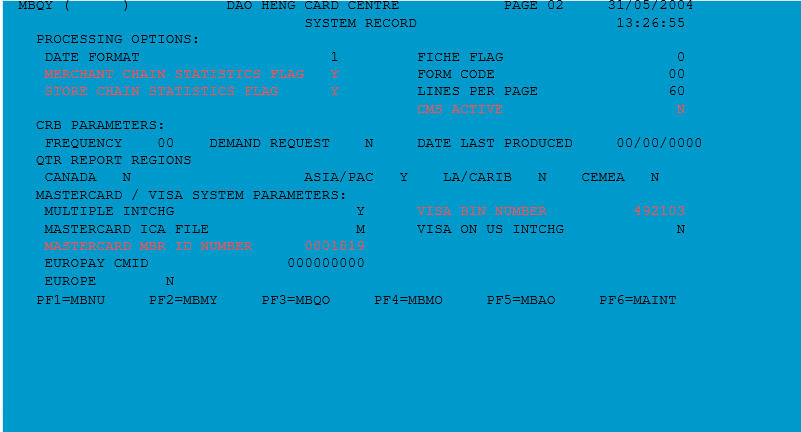

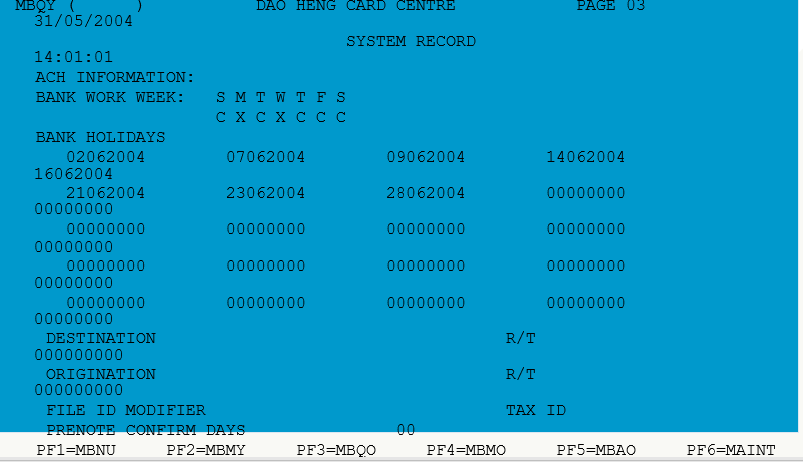

A collection of options and parameters which control the processing of the system, defined and maintained online, CMS consists of 25 control records.

▲Provide logical groupings based on Hierarchy of Business Controls

▲Primary Records

System levels control Processing Dates, system holidays and Interfaces.

Org level controls area of business, billing dates, ACH information, activity recap controls etc. Logo Level controls Account Processing Options like Payment options, account type etc.

▲Secondary records

Control the processing parameters like Interest rates, Insurance and account records

CMS has 22 secondary records which can be established as options under a controlling System, Organization or Logo record.